Is 150 too many?

May 10, 2023

By Jill Edmonds

For nearly the past two decades, prospective CPAs in Virginia have had to undertake 150 hours of education before becoming licensed. But a declining CPA pipeline has accountants asking: Is the 150 now a barrier to becoming a CPA? Is it time to reimagine how we prepare CPAs for an increasingly evolving profession?

VSCPA members — CPA leaders across organizations of all sizes — are asking these questions. In September 2022, the VSCPA Board of Directors convened a special 150-Hour Task Force to gather data on the 150, review challenges to the CPA pipeline, and make a recommendation to the Board on if the VSCPA should change its standing position supporting the 150-hour requirement for licensure.

Between the 1970s and 2020, every U.S. state and territory adopted the 150-hour educational requirement, an increase from 120 hours. As early as 1956, a Commission on Standards and Experience for Certified Public Accountants Report stated a graduate degree would be preferable for accountants.

“As leaders in the profession began to review educational requirements, they saw distinct advantages to requiring 150 hours,” said Stephanie Peters, CAE, VSCPA president & CEO. “They identified that the CPA profession was marked by high-quality, knowledgeable accountants who were committed to personal integrity and ethics. They believed requiring more education would set them apart from their unlicensed counterparts.”

Additionally, 150 hours was thought to increase CPA Exam success rates and attract the brightest talent to a prestigious profession.

In 1979, Florida became the first state to pass legislation requiring 150 hours, which became effective in 1983. By 1988, the American Institute of CPAs (AICPA) required new members after 2000 to have completed 150 hours. And in 1990, the AICPA and National Association of State Boards of Accountancy (NASBA) developed model rules to implement the requirement. Flexibility to obtaining 150 was urged to encourage non-traditional accountant students to enter the CPA profession.

The initiative really gathered steam in the 1990s, with dozens of states passing and enacting 150. Virginia passed it in 1999 as part of adopting the Uniform Accountancy Act model rules, with a 2006 effective date. By that point, many firms were only hiring CPAs who had completed 150 hours because they had cross-border work, and standards were different depending on the state. It became clear that substantial equivalency was necessary to ensure the stability of the profession.

Substantial equivalency allows CPAs from any jurisdiction to practice across borders as long as the states have similar education, experience and Exam requirements.

By the early 2000s, states began to roll back the 150 requirement to sit for the CPA Exam. Currently 43 states, including Virginia, allow 120 hours to take the Exam but candidates still need to fulfill their 150 hours before becoming licensed.

There are a variety of different paths to getting to 150 hours of education. Some students acquire a master’s degree in accounting or business or an MBA. Others may build expertise in certain content areas by obtaining graduate certificates. Still another path is to double major in an undergraduate program and take additional coursework to get to 150. Nontraditional paths are allowed to obtain the required educational requirements, and there is flexibility.

Back in 2008, NASBA issued a discussion document about the 120-hour Exam-sitting requirement. The organization wrote, “Adoption of the 150-hour requirement was not done in haste. The quest for the 150-hour education requirement goes back to the time when NASBA was called the Association of CPA Examiners and the American Institute of Accountants (AIA) was still not a part of the AICPA. The requirement was brought about by many factors, including: the expansion of client services, the growing application of information technology (electronic data processing), the increase in accounting pronouncements, the recognition of the value of formal education over informal experience, and the desire for the recognition of accounting as a profession at least as demanding as law, engineering and architecture.”

The genesis of educational requirements for CPAs makes sense. But two decades into a new millennium, things are changing — starting with basic numbers.

College enrollments are dropping

Before you can even discuss the number of accounting majors, you must review the stark numbers on college enrollment overall, and it’s not pretty.

According to the National Center for Education Statistics and National Student Clearinghouse Research Center, between the fall of 2012 and the fall of 2022, the number of students enrolled in college dropped almost 10%, or nearly 2 million. The trend of declining enrollment accelerated during the pandemic, with nearly 8% dropping between 2019 and 2022.

This is not to say that college is no longer popular. While some people re-evaluated their career paths in light of the pandemic, dropping enrollment can also be related to declining birth rates.

Colleges and universities are acutely aware of an “enrollment cliff” expected in 2025. In that year, the college-age population will dramatically drop due to the plummet of babies born between 2008 and 2011 (the Great Recession). In 2025, 576,000 fewer students will enter college.

Fewer students are choosing accounting

With fewer students overall, that means fewer accounting majors. And it’s important to note: The CPA profession is not the only prestigious credential fighting for talent. Doctors, lawyers, engineers … Everyone wants the best students, and all professions are trying to attract the brightest minds to their fields. Among this competitive environment, students are reviewing the data: Which fields hold the greatest career promise? Which choices yield the highest salaries?

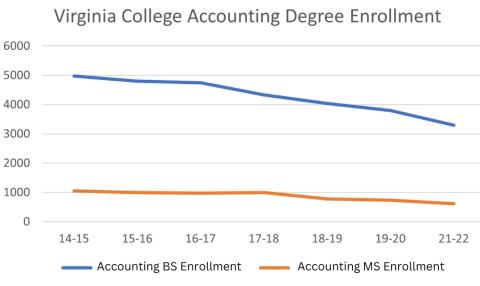

Nationally, student enrollment in accounting programs has been on the decline since 2016. That trend holds true for Virginia as well (see Figure 1 below). Consequently, fewer CPA firms are able to hire accounting graduates, and more non-accounting graduates are filling jobs formerly held by CPAs.

Figure 1

The 2021 AICPA Trends Report, the most recent study of the supply and demand for accountants, found that accounting graduates trended downward in the 2019–2020 academic year (the most recent year that data was available), with declines of 2.8% in bachelor’s accounting graduates and 8.4% of master’s grads.

Fewer students are sitting for the CPA Exam

As expected, the trickle-down effect from fewer college students to fewer accounting majors means fewer CPA Exam takers. The 2021 Trends Report found that while the number of CPA Exam candidates decreased less than 0.5% between 2018 and 2019, there was a 17% decrease between 2019 and 2020. With Exam testing centers closed due to the pandemic, this was to be expected. The profession is closely watching for Exam candidate numbers to rebound, as a 6% increase occurred between 2020 and 2021. Still, numbers are significantly lower than before the pandemic.

Statistics from the Virginia Board of Accountancy (VBOA) reveal Virginia licensees in June 2022 were down 2% year-over-year. In that same period, inactive licensees grew 2.5% and are up 15% since 2019. CPA candidates decreased 6% since June 2021 and 33% since 2020.

A 2021 special report on the CPA pipeline from the Illinois CPA Society, Decoding the Decline, surveyed more than 3,000 accounting students and young CPAs to decipher the challenges the profession faces. Respondents said the largest barrier they faced to becoming a CPA was the time commitment needed to study for and pass the CPA Exam.

Additionally, among respondents who did not plan on becoming CPAs at all, 32% said they did not see the CPA credential as providing value or relevance to their careers, and 28% didn’t believe they would see a return on investment.

The hiring landscape is ultra-competitive

These statistics are having a real and lasting impact on CPA firms and corporate finance teams who depend on CPAs to do the high-level, strategic accounting and financial work needed by their clients and businesses. In 2023, everyone who wants a job has a job; the overall national unemployment rate is 3.5%, and Virginia’s is even lower at 2.8%.

The cutthroat hiring environment naturally has CPAs asking: If the 150-hour requirement were gone, would more candidates find the CPA designation attractive? That’s certainly a solution being discussed in various parts of the country.

To truly analyze the issue and dig deep into the data, the VSCPA Board of Directors wanted to find out.

Under the direction of 2022–2023 Board Chair George Forsythe, CPA, the 150-Hour Task Force convened to develop a draft position to present to the Board at its January meeting, with the ultimate goal of the Board voting on the position in April.

The Task Force comprised Board representatives and VSCPA Diversity, Equity & Inclusion (DEI) Advisory Council members, as well as other members and educators and a representative from the Virginia Board of Accountancy.

“Juggling the demands of the profession, along with limited capacity and scarce staffing resources, is the top issue right now facing firm and industry leaders,” George said. “Chatter has begun swirling nationally indicating negative impacts of the 150-hour requirement. Empowering our members to thrive is the primary focus of VSCPA Board and staff, thus, we readily embraced this issue to resolve whether the 150-hour rule is creating barriers to entry.”

Damon DeSue, CPA, a previous Board of Directors chair and member of the DEI Advisory Council, agreed to helm the Task Force. “I have deep concerns about the pipeline and the barriers we are self-creating for entrance into the profession,” Damon said.

The group met four times last year to facilitate a robust and thoughtful discussion on the impact of the 150-hour requirement. The Task Force evaluated historical data, reviewed relevant statistics, surveyed VSCPA members about their thoughts and experiences, and spoke with students, experts, and other stakeholders. The Task Force considered if the VSCPA should maintain its position of support for 150 and if the VSCPA should actively work to influence the 150-hour requirement in Virginia or nationally.

To formulate its recommendation, Task Force members took a deep dive into the below areas.

VSCPA member survey data

In December 2022, the VSCPA conducted a survey of members to determine their perceptions of the 150-hour requirement — and they do believe it’s a barrier.

Respondents identified these as the three strongest, potential barriers to the profession: time needed for CPA candidates to take additional 30 hours of education, cost of additional 30 hours, and impression of a CPA’s workload. Conversely, members do not believe that starting salaries are a barrier; that ranked much lower on the list.

Approximately half (48%) believe the 150-hour requirement has not improved the quality of job candidates, and only 22% have seen a little or moderate improvement. As one respondent said, “I’m not convinced there is a difference, and I have a master's of accountancy degree. I teach masters’ students at a university. My undergrads are often more attentive and do better work.”

As a solution, a majority, 63%, are either interested or very interested in eliminating the 150-hour requirement. “Additional hours of school does not deliver better employees,” says one member. But of those not in favor, there are concerns: “Going backwards will dilute the profession,” says another.

Damon said he wasn’t surprised by members’ feedback. “CPAs in general have a big concern about the pipeline. They are the ones seeing what the universities are producing. They are not confident the pipeline can be sustained.”

Other data of CPA’s perceptions of the 150 have similar results. In a 2022 INSIDE Public Accounting survey to public accounting firm leaders of varying sizes, 81% said they thought the 150 hindered their firms’ abilities to recruit accounting graduates. Nearly three-quarters said they still couldn’t find candidates with the analytical skills their firms need.

Studies on the 150’s effects on the profession

A few academic studies have investigated how the 150-hour requirement affected the overall pipeline. In 2019, the University of Chicago Booth School of Business revealed the number of first-time Exam candidates dropped by 15% after the 150 was implemented. Additionally, a 2020 working paper from Utah State University identified the 150 as a barrier to entry. Both papers did not find that 150 hours led to increased candidate quality.

But if you ask young and prospective CPAs, you’ll find different answers. The Illinois study discovered the cost of obtaining the extra 30 credit hours to become a CPA was not a significant challenge at all. Neither new CPAs, those in the process of becoming a CPA or planning to, those who abandoned the process, nor students identified the 150 as a significant barrier. What is? The workload and personal time commitments to study for and take the CPA Exam. Whether or not a CPA candidate takes 120 hours or 150 hours, the daunting task of facing the CPA Exam is the biggest challenge — and that won’t ever go away.

“The common assumptions that the costs associated either with obtaining the additional credit hours to meet the educational/licensing requirements or preparing for and taking the CPA exam are top barriers were proven to be misconceptions — these were not the top barriers cited among any respondent category,” the report states. “In fact, these factors were ranked lower than we anticipated, which was interesting given how much emphasis we often place on them and how many resources we create to help deal with these expenses.”

VSCPA member survey data shows that Virginia CPAs are concerned about the 150 as a time and cost barrier, but the Illinois study indicates those fears could be misconceptions.

The reality of business

Since the 150-hour requirement went into effect, a lot has changed in the professional environment. When the discussion of increasing educational requirements began in earnest in the late 1980s and early 90s, the Sarbanes-Oxley Act wasn’t a glimmer in anyone’s eye. Here are just a few of the many realities the profession and businesses now face:

Coupled with new areas of focus like environmental, social and governance (ESG) reporting, financial planning & analysis (FP&A), and a myriad of technological changes including robotic process automation (RPA) and artificial intelligence (AI), today’s businesses need employees with cutting-edge skills and experience.

The impact on attracting minorities to the profession

Increasing the diversity of the CPA profession is a consistent goal of accounting organizations nationwide, and the Task Force didn’t want to overlook the potential negative ramifications the 150-hour requirement could have on recruiting diverse accounting talent.

The 2021 Trends Report shows that, while slow, the needle is moving. Hiring of new, diverse bachelor’s and master’s degree graduates increased by almost five percentage points during the 2019–20 and 2020–21 academic years. A wide array of programs on the state and national levels are making an impact, but organizations must continue to make diversity a priority to continue the positive trend.

As investigated by the VSCPA DEI Advisory Council, there are many barriers minorities face when trying to enter the profession: lack of awareness about accounting, complexity of navigating college, cost, and more. The Illinois survey discovered higher percentages of minority respondents must pay 100% of their CPA Exam fees than their white counterparts, highlighting a need for further financial support by employers.

Multiple organizations and reports continue to highlight the accounting diversity challenge and offer solutions. (The Center for Audit Quality’s Accounting+ initiative is one example of how the profession is responding.)

Salary data

As demand grows for professionals in data analytics, cybersecurity, and other hot fields, talented college students may be choosing careers other than accounting. There are concerns that starting salaries for new accountants aren’t as competitive as those in other fields.

“If I’m a student nowadays,” Damon said, “I’m going to be asking, ‘Is it going to pay to get my CPA?’” The compensation increase for someone who obtains their CPA license is not drastic, he says. After students pay for education, many of them (and their parents) review the cost-benefit of what that degree will equate to in real-world wages.

The 2022 VSCPA Compensation & Benefits Survey does show that new hires and young accountants in Virginia are receiving higher salaries than before the pandemic. Firms are increasing fees and offering more competitive starting salaries. But these still must keep pace, or even exceed, other fields to attract the best talent.

Any time a major licensing requirement changes, there are risks to the health of the profession. The Task Force discovered a significant detractor to rolling back the requirement to 120: CPA mobility. Currently, Virginia CPAs have no issues with mobility. Because all states have adopted substantial equivalency, CPAs can easily practice across state lines.

Ultimately, the Task Force decided the risk to Virginia’s CPAs was too great for just a statewide 120-hour mandate. But that shouldn’t be the end of the conversation.

The draft position the Task Force presented to the Board for consideration reiterates the VSCPA’s previous position in support of substantial equivalency. However, the Task Force believes it’s also clear the 150 does not meet the profession’s expectations overall — and must be redefined.

In April 2023, the Board of Directors evaluated and passed the below strike and addition to its position:

The Society endorses substantial equivalency and practice mobility as established under the Uniform Accountancy Act (UAA). This includes maintaining the UAA minimum requirements for examination, education (150 hours), and experience for licensure. The Society further endorses redefining the education requirement and advocating for a combination of traditional course work and/or other approved programs and experience relevant to the newly licensed CPA. In addition, CPAs from other states should be permitted to practice in Virginia under the substantial equivalency doctrine.

Additionally, the VSCPA set specific pipeline-related goals for 2023–2024:

Before beginning the Task Force’s work, Damon said, “I don’t think I had the depth or appreciation for how entrenched the 150 is in our profession. I did learn more about the origin.” After review, he said it became clear that the profession does need to have something that requires a higher standard of learning.

“If we are going to be objective and do what’s in the best interest of the profession,” said Task Force member Brandon Pope, CPA, “We need to realize that the 150, as it’s now implemented, poses significant challenges to furthering the profession’s growth.”

As many members pointed out in the VSCPA survey, the lack of direction to the extra 30 credit hours needed does not adequately train CPAs. Says one, “In Virginia, the extra 30 hours can be taken in any subject. That means the candidate is no better prepared than they would be at 120 hours. If we are going to require 150 hours, it would be better to require a master’s of some sort. As experience is more valuable than schoolwork (after you learn the basics), having internship hours would add way more than classwork.”

That member’s feedback is just one way the 150-hour requirement could be shaped. And that conversation needs to happen at a national level so the entire profession is on board.

Task Force members did not come to this recommendation lightly. Some members were adamantly against supporting the 150, but after reviewing the data, realized the importance of maintaining substantial equivalency.

In Virginia, we wanted to listen to our members and then have an open dialogue about the future of the 150 requirement and how it could be shaped to better meet the needs of a changing profession. CPAs in other states are asking similar questions, and other states have their own solutions.

The Indiana CPA Society also has a Board task force looking at the 150-hour requirement and other barriers to entry. The Minnesota Society of CPAs created legislation to return their state's requirement to 120 hours while increasing the experience requirement to two years. While this decision has been sharply criticized by the AICPA, Minnesota believes such a move is in the best interest of its CPAs.

The AICPA sees any legislation to make changes to the 150 as undermining the integrity of the CPA license. Instead, it’s focusing on initiatives to increase the CPA pipeline via a draft Pipeline Acceleration Plan. Elements of its multi-part plan include implementing an Experience, Learn & Earn (ELE) program to help candidates get their final credit hours, addressing firm culture and business model challenges, implementing a 30-hour communications and awareness campaign, extending the 18-month Exam window, and tackling inconsistencies in state licensure pathways. The AICPA is actively seeking feedback from stakeholders on the acceleration plan. The VSCPA has already submitted comments and will remain involved in national initiatives focused on the pipeline.

The Big Four accounting firms have each made their own investments in promoting accounting careers, from funding scholarships to acceleration programs. EY offers a career path accelerator plan that allows its prospective CPAs to take their extra 30 course credits virtually at Hult International Business School plus experience hands-on learning at the firm. PWC has a similar program with an online master’s degree offered via Northeastern University and also offers a partnership with Saint Peter’s University in New Jersey that doesn’t require getting a master’s.

It’s clear the 150-hour requirement is not currently meeting the profession’s expectations. What we need to do now is figure out a way — on a national level — to review the requirement so that it is meaningful and provides value.

The VSCPA believes CPAs can protect mobility and substantial equivalency while reviewing if the 150-hour requirement in its current iteration in the UAA is the best path forward. Nationally, CPAs must consider if the extra credit hours need to be better defined, or if experience can stand in for some credits.

“There is no ability to push this under the rug,” Damon said. “The conversation is here to stay.”

The VSCPA plans to be a part of it.

Jill Edmonds, VSCPA communications director, has acted as managing editor of Disclosures magazine for the last 20 years. In addition to the magazine, she oversees the Society’s content and communications strategies. She loves a good, color-coded planning spreadsheet.

CHAIR: Damon DeSue, CPA, CGMA, PRA Group, Inc., Norfolk

JJ Edmunds, CPA, PBMares, LLP, Richmond

Milly Ikundi, CPA, McKinsey & Company, Washington, D.C.

LaToya Jordan, CPA, CGFM, Auditor of Public Accounts, Richmond

Jeffrey Kum, student, Virginia Commonwealth University, Richmond

Gabriele Lingenfelter, CPA, Christopher Newport University, Newport News

Andrew Martin, CPA, Corbin & Company, PC, Chesapeake

Kelli Meadows, CPA, Meadows Urquhart Acree & Cook, LLP, Henrico

Darry Newbill, CPA, Deloitte, Richmond

Jim Phillips, CPA, KPMG, Richmond

Brandon Pope, CPA, Vaco LLC, Richmond

Nadia Rogers, CPA, CGMA, Virginia Tech, Blacksburg

Jamil White, CPA, New Energy Equity, LLC, Annapolis, Md.